Investing | Article

Why It’s Important to Save $100,000 by 30

by The Simple Sum | 13 May 2021 | 5 mins read

When discussing personal finance, a certain magical number will almost always come up: 100,000. Why are financial advisors and finance gurus out there so obsessed with this number? Well, it’s actually pretty special.

To pique your interest, let’s look at the math and crunch some numbers.

Why is $100k SUCH a big deal?

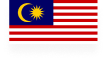

If you saved $1,000 a month and put those savings into an investment that returns 5% annually, you’ll have grown your savings to $100,000 in seven years and two months. Say you start work at 22 years old, by saving $1,000 a month, you would hit that magic $100,000 by the time you reach 30.

Saving $1,000 a month feels like a lot, especially in your 20s. But by saving and investing this amount earlier in your life, you’ll take less time to get to your next $100,000. All thanks to the power of compounding!

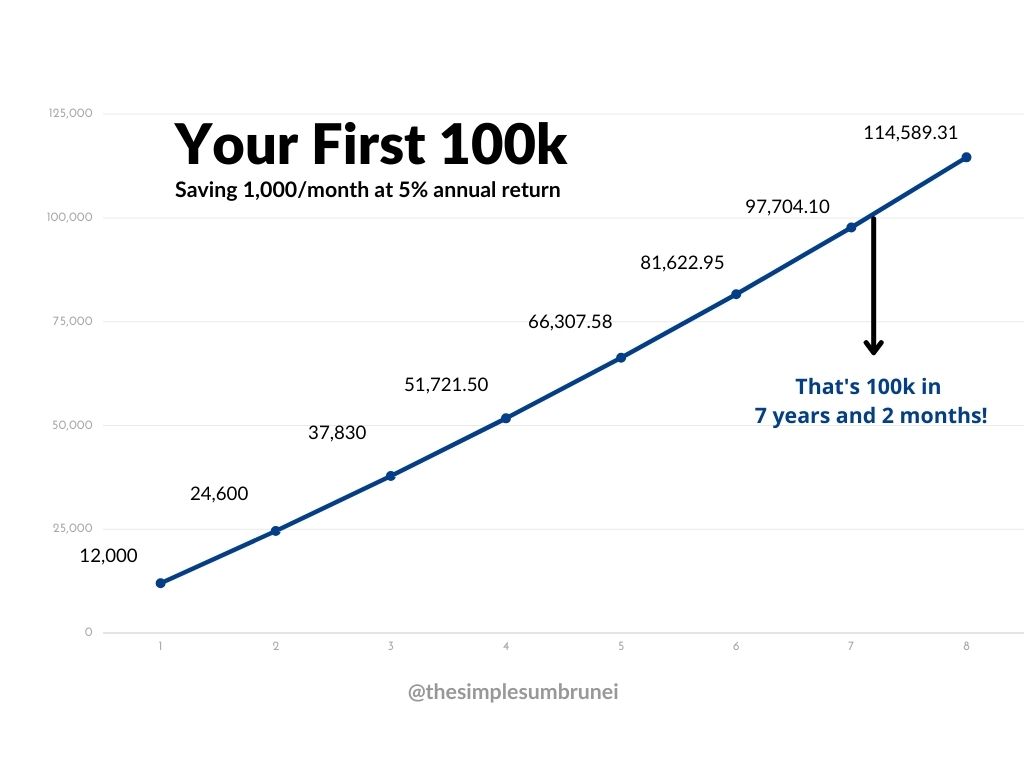

In fact, the power of compounding cuts down the time you need to get to $200,000 from seven years to only five years! (Not to mention, you don’t have to save as much money to get to $200,000).

If you keep on saving $1,000 a month throughout your life, you’ll begin to see a snowball effect in your interest earnings.

Most of your first $100,000 comes from the effort you put by saving. In our example, 83% (or $96,000) of the $114,589.31 you’ve accumulated in year 8 is your own savings. The remaining $18,589.31 is the gain from investing your savings.

But after that initial $100,000, you only need to save an additional $60,000 for 5 years to get to $212,555.79. So, instead of taking seven years to get to the next $100,000, you only need five years. And instead of having to save $96,000, you only need to save $60,000.

At this trajectory, by the time you retire at 60, assuming you start work at 22, you’ll have a cool $1.2 million in savings – just by saving $1,000 a month!

This is why every finance guru harps on this magical number of $100,000.

The best place(s) to start saving

Business man and shark enthusiast Shark Tank star Kevin O’Leary says that by the time you’re 33, you should have $100,000 saved somewhere.

When you’re just starting at your first job, saddled with debt, and earning something like $2,000 a month, it may seem impossible to have $100,000 by the time you’re 30.

But let’s not forget that we have our TAP funds to rely on as well, to build our long-term savings. According to the law, our income contributions to TAP will be 5% of our basic salary.

On top of that, our employers are obligated to contribute another 5% to our TAP, making it a total of 10% of our basic salary going into the pension scheme every pay cycle!

So, for example, if you’re earning $2,000 a month, then the total TAP contributions you’re getting will be $200 a month. After that, all you have to do is top up $800 to hit your monthly savings target of $1,000.

Of course, progress won’t be so linear – especially when you consider that your salary will likely increase as you progress further in your career.

This way, you’ll ensure you have $100,000 saved somewhere by the time you hit 30.

But saving $100,000 by 30 still sounds impossible

We’ll put your mind at ease: 30 is just an arbitrary number. Sure, we can all aspire to achieve this milestone by 30 but if you can’t get to $100,000 by that age, that shouldn’t put you off from saving and investing.

While saving $100,000 is important, we also understand that it may be difficult to some.

If you’re 30 and just now finding out about this concept, maybe have a peek at your TAP account. Does your TAP need some help getting to $100,000?

If you’re still a long way from that $100,000 mark in your TAP account, divide your payments (to yourself) into manageable chunks and see if you’d still like to increase those contributions once your salary increases. Your future self will thank you.

If you’re in your early 20s and you’re struggling to save money because you don’t earn a lot of money, then make use of your best assets: time and energy. Use your time and energy for side hustles or developing new skills.

Or simply spend less, avoid debt, and live within your means.

Of course, your quality of life is certainly more important than the quantity you have in your bank account; eating instant noodles for every meal and stealing your neighbour’s Wi-Fi is no way to live.

So, even if you don’t get to $100,000 by 30, that’s fine. Just think of it as a goal that you’d like to get to at some point in your life. As long as you get into the habit of saving consistently, you’ll eventually get there.

It’s simple – every little bit counts

To put it simply, save as soon as possible and save as much as possible. If you feel like the pressure to save is too much, let some months go by without saving and catch up in the following months.

More than accumulating wealth, the goal of saving $100,00 is about cultivating a healthy habit of saving and taking charge of your finances.

If you’ve already saved $100,000 (or more) on your own, drop us an email! We’d love to tell your story.